credit.suarajatim.com

credit.suarajatim.com

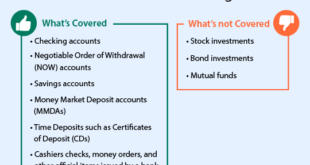

Credit Union Overdraft Protection: Why You Need It. Credit union overdraft protection is a service that helps members avoid declined transactions, returned checks, and overdraft fees by covering shortfalls in their accounts. When an account lacks sufficient funds, the credit union steps in to cover the deficit using linked accounts, lines of credit, or overdraft privilege programs.

How Does Credit Union Overdraft Protection Work?

Overdraft protection can function in several ways depending on the credit union’s policies:

- Linked Savings or Checking Accounts – Funds are transferred automatically from a linked account to cover an overdraft.

- Overdraft Line of Credit – A credit line is attached to your checking account, automatically covering negative balances up to a set limit.

- Overdraft Privilege – The credit union temporarily covers the overdraft up to a certain amount, which must be repaid with applicable fees.

Benefits of Overdraft Protection

- Avoid Overdraft Fees – Reduces or eliminates costly penalties.

- Prevents Transaction Declines – Ensures payments go through smoothly.

- Improves Financial Flexibility – Gives extra time to cover unexpected shortfalls.

- Protects Your Credit Score – Helps avoid missed payments that could affect credit.

- Provides Peace of Mind – Reduces stress about insufficient funds.

Credit Union Overdraft Protection vs. Bank Overdraft Protection

Credit unions often provide more member-friendly terms compared to banks. Banks may charge higher fees and offer less flexibility, while credit unions typically have lower fees and more forgiving policies.

How to Enroll in Overdraft Protection

- Check with Your Credit Union – Contact a representative to learn about available options.

- Choose the Best Protection Plan – Decide whether a linked account, line of credit, or overdraft privilege suits your needs.

- Review Terms and Fees – Understand costs and repayment requirements.

- Opt-In if Required – Some credit unions require members to opt in for overdraft privilege programs.

Costs and Fees of Overdraft Protection

Fees for overdraft protection vary but may include:

- Transfer Fees – A small fee per transaction when funds are moved from a linked account.

- Interest on Overdraft Lines of Credit – Interest applies when borrowing from an overdraft credit line.

- Overdraft Privilege Fees – Charges for covering transactions temporarily.

Risks of Overdraft Protection

- Potential for Overuse – Relying on overdraft protection frequently may lead to financial instability.

- Fees Can Add Up – Even small fees can accumulate if overdrafts happen regularly.

- Possible Credit Impact – Unpaid overdraft lines of credit may affect credit scores.

10 Tips for Managing Overdraft Protection Wisely

- Set up low balance alerts to monitor account activity.

- Maintain a financial cushion in your checking account.

- Use a budget to track income and expenses.

- Avoid relying on overdraft protection as a financial safety net.

- Understand the specific fees associated with your overdraft protection.

- Link a savings account to minimize overdraft charges.

- Pay off overdraft lines of credit quickly to reduce interest costs.

- Review account statements regularly to identify overdraft patterns.

- Opt for a credit union with lower overdraft fees.

- Consider alternative banking solutions like prepaid debit cards to avoid overdrafts altogether.

10 Frequently Asked Questions About Credit Union Overdraft Protection

1. Do all credit unions offer overdraft protection? Not all credit unions offer overdraft protection, so it’s important to check with your institution.

2. Can I opt out of overdraft protection? Yes, most credit unions allow members to opt out of overdraft services.

3. Does overdraft protection affect my credit score? Only if an overdraft line of credit is used and payments are missed.

4. What happens if I don’t repay my overdraft? Unpaid overdrafts may result in account closure, collection efforts, and credit score impact.

5. Can I have multiple overdraft protection options? Some credit unions allow members to use a combination of linked accounts, credit lines, and overdraft privileges.

6. Are overdraft fees refundable? In some cases, credit unions may refund fees for first-time overdrafts or special circumstances.

7. How much can I overdraft with overdraft protection? The limit depends on your credit union’s policy and the type of overdraft protection.

8. Do I need good credit for an overdraft line of credit? Yes, approval for an overdraft line of credit typically requires a credit check.

9. Does overdraft protection cover ATM withdrawals? It depends on the credit union and whether you’ve opted into coverage for ATM transactions.

10. How do I cancel my overdraft protection? You can cancel overdraft protection by contacting your credit union and requesting removal.

Conclusion

Credit union overdraft protection is a valuable financial tool that can help members avoid declined transactions, returned checks, and costly fees. By understanding how overdraft protection works, the costs involved, and how to use it responsibly, members can take advantage of the benefits while minimizing risks.

Choosing the right overdraft protection strategy requires evaluating your financial habits and banking needs. Whether you link accounts, set up a line of credit, or use overdraft privilege services, managing overdraft protection wisely ensures financial security and peace of mind.